Paisabazaar-Check your credit score

Paisabazaar-Check your credit score

Credit score Rating is a 3-digit quantity that represents your creditworthiness. This rating ranges between 300 and 900 and is calculated foundation your track-record of previous loans and bank cards. A excessive credit score rating, often over 750, is most well-liked by banks and different lenders to supply new loans and bank cards. Shoppers can test their credit score rating totally free right here, with month-to-month updates, from a number of credit score bureaus, together with CIBIL. This may be handled as a delicate enquiry, may have no impression in your rating and comes with simple month-to-month monitoring that ought to assist to construct your credit score rating.

Credit score rating is supplied by credit score bureaus, together with CIBIL or Credit score Data Bureau (India) Restricted. Also called TransUnion CIBIL, it's India’s oldest Credit score Data Firm (CIC). CIBIL, like different credit score bureaus viz., Experian, Highmark and Equifax, collects and maintains credit score data of all Indian debtors, as reported to them on a month-to-month foundation by banks, NBFCs and different institutional lenders. Anybody, who has taken any form of mortgage or bank card, may have a CIBIL Rating, which is scored out of 900.

What's CIBIL Rating & CIBIL Report?

TransUnion CIBIL each month receives particulars from lenders on how customers are behaving with credit score (loans and playing cards); this features a new software for credit score merchandise, reimbursement track-record of EMIs on current loans and bank card payments, present excellent debt, how a lot of their bank card restrict or credit score line is being utilized and many others. Foundation this data, an in depth month-to-month CIBIL Report for every shopper is generated which features a CIBIL Rating.

The importance of CIBIL Rating is that it's utilized by lenders to evaluate a borrower's creditworthiness for brand new loans and playing cards. Everytime you apply for any mortgage or bank card, your CIBIL Rating is among the first issues a lender will have a look at whereas processing your mortgage software.

A powerful CIBIL Rating (usually above 750) denotes a robust credit score historical past and banks and different lenders choose such customers for his or her loans and bank cards as they've a very good observe report of accountable behaviour with credit score. Alternatively, a poor CIBIL rating (usually beneath 600) is perceived by lenders as 'dangerous'; customers, with a poor credit score rating, are both rejected for brand new loans and bank cards or are provided a lot increased charges of curiosity.

We, therefore, advocate that each one customers ought to test and observe their CIBIL rating recurrently. This may assist them perceive good credit score behaviour that will assist them construct their CIBIL Rating over time. Checking and monitoring their credit score rating on Paisabazaar.com is free and fully digitized.

Shoppers ought to observe that CIBIL report or Credit score Report from any credit score bureau solely takes into consideration the dealing with of credit score devices. Different monetary devices reminiscent of your internet value (financial institution steadiness, investments, annual wage, enterprise turnover, and many others.) play no position in how excessive or low your credit score rating shall be.

Eligibility to test CIBIL Rating

Any Indian citizen can test their CIBIL rating, topic to the next 2 situations:

- Solely those that have taken a mortgage or bank card of their previous may have a CIBIL Rating. You probably have by no means taken any form of credit score product, then you're "new to credit score" and won't have a CIBIL or Credit score Rating

- It is best to have a legitimate PAN Card which was supplied by you to the lender whereas availing credit score up to now

The above are obligatory necessities and your CIBIL rating and report is not going to be generated except each these situations are met.

Elements affecting your CIBIL rating

CIBIL Rating is calculated utilizing the credit score historical past present in your CIBIL Report. It displays an individual’s credit score behaviour which incorporates frequency of making use of for loans/bank cards, credit score reimbursement historical past, mixture of secured and unsecured credit score, and many others. Usually a rating nearer to 900 is taken into account to be a very good rating. Some elements which have an effect on an individual’s CIBIL rating are given beneath:

1. Compensation Historical past: Mortgage reimbursement historical past like well timed fee of your bank card payments and EMIs (equated month-to-month installments) impacts your CIBIL rating. Lacking well timed funds of your bank card payments or EMIs tends to adversely impacts your CIBIL rating and thereby your capacity to safe new credit score sooner or later.

2. Credit score Utilization Ratio: Credit score Utilization Ratio is calculated by dividing the quantity of credit score availed by the accessible credit score restrict. A excessive credit score utilization ratio signifies a heavy reimbursement burden that negatively impacts your CIBIL rating. An individual with a low credit score utilization ratio (30% or decrease) has increased credit score worthiness for lenders and may avail further credit score with better ease.

3. Simultaneous Mortgage/Credit score Card Purposes: Purposes for brand new bank cards/loans set off onerous enquiries from potential lenders. These enquiries present up in your CIBIL report which adversely impacts your CIBIL rating is a number of onerous enquiries present up in your report concurrently.

4. Credit score Combine: It's good to have a balanced mixture of secured and unsecured loans. Having an excessive amount of unsecured debt within the type of bank card debt and excellent private loans adversely impacts your CIBIL rating. It's because such credit score behaviour is usually interpreted as an indication of mismanagement of private finance. Having a mixture of secured loans (like Auto and Dwelling loans) and unsecured loans, will help you preserve a excessive CIBIL rating and improve probabilities of availing new credit score.

5. Growing Credit score Card Restrict Incessantly: Making frequent requests for rising the credit score restrict in your bank cards might improve the variety of onerous inquiries. This may increasingly adversely have an effect on your CIBIL rating because it may be perceived as excessive dependence on credit score by potential lenders resulting in an elevated probability of default sooner or later.

6. Errors in Credit score Report: Errors in CIBIL studies reminiscent of an incorrect point out of default in repayments, wrongly assigned loans/bank cards, errors in private data, and many others. might adversely have an effect on your CIBIL rating. Moreover, incorrect or delayed reporting by banks might also negatively impression your CIBIL rating.

7. Lack of Credit score Historical past: Your CIBIL rating is calculated on the idea of your credit score behaviour, mortgage reimbursement historical past, credit score utilization restrict, and many others. Absence of credit score historical past negatively impacts your CIBIL rating. It turns into tough for the lender to find out the danger class the person falls into in case he/she has by no means taken a mortgage or by no means had a bank card.

8. Incapability to meet your position as a mortgage guarantor: Changing into a guarantor for any person else’s mortgage makes you liable to pay the mortgage in case he/she fails to take action. The guarantor’s CIBIL rating is impacted in case he/she fails to repay a mortgage the place the first borrower has already defaulted.

Forms of Credit score that impacts your credit score rating

Loans can primarily be divided into 2 classes - secured loans and unsecured loans. Secured loans reminiscent of auto loans, dwelling loans, and many others. are secured by collateral (safety). Whereas, unsecured loans like bank cards and private loans may be availed with out collateral/safety.

Having a balanced mixture of secured and unsecured loans (credit score combine) favourably impacts your credit score rating and will increase your probabilities of availing new credit score.

Alternatively, having too many unsecured loans adversely impacts your credit score rating and the possible lender perceives the next danger in lending cash to such people.

On-line Portals to Test your CIBIL Rating

Whereas CIBIL report generated by TransUnion CIBIL may be accessed on-line from the cibil.com web site, there are different on-line portals that you need to use to entry the identical. These embrace official CIBIL companions like Paisabazaar.com who present entry to your credit score report and credit score rating. Whereas Paisabazaar gives you entry to your credit score report freed from cost, different CIBIL companions might or might not supply the identical service totally free.

Methods to test your CIBIL Rating for Free

Clients can test their CIBIL rating on-line with out paying any further fees. They will accomplish that both by visiting the official web site of Paisabazaar or via the official CIBIL portal.

Test On-line at Paisabazaar

The steps to test your CIBIL rating via paisabazaar.com are given beneath:

- Go to Paisabazaar.com

- Click on the “Get Report” button on the house web page.

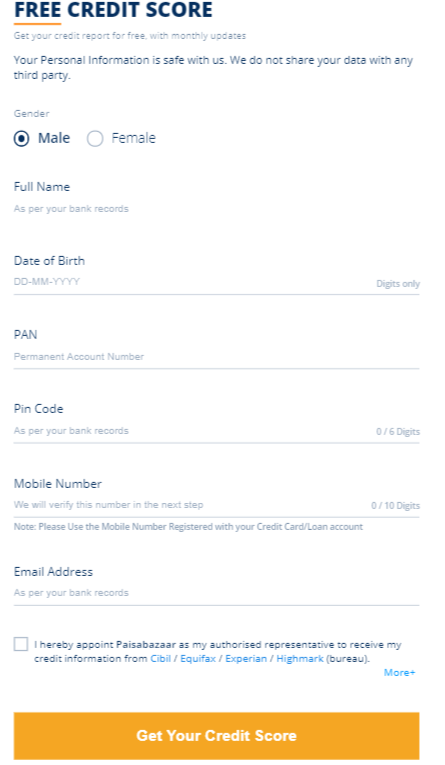

3. On the web page that opens subsequent, fill in particulars like your gender, title, date of beginning, PAN, and many others. , then click on the checkbox to agree with phrases and situations.

4. Click on on ‘Get Your Credit score Rating’. You may be knowledgeable by electronic mail and SMS when your credit score report and rating has been generated. The report shall be accessible and accessible for obtain via your free Paisabazaar.com account.

Test on Official CIBIL Web site

Clients can even test their CIBIL rating by visiting the official web site of TransUnion CIBIL. The steps to test your CIBIL rating via CIBIL.com are:

- Go to CIBIL.com

- Click on on ‘Get Yours Now’.

- Fill in private particulars like electronic mail id, PAN, title, and many others. to create your account.

- You'll obtain a verification mail, following which you'll be required to substantiate some particulars like your passport quantity, driving license quantity, and many others.

- Upon profitable verification, you're going to get your CIBIL rating.

How CIBIL Rating is Calculated?

CIBIL has its personal proprietary algorithm to calculate an individual’s credit score rating and the precise extent to which a person issue impacts the CIBIL rating just isn't at the moment recognized. Nonetheless, some key elements that affect an individual’s CIBIL rating are as follows:

- Mortgage reimbursement historical past: Defaulting in your EMIs or making late funds negatively impacts your CIBIL rating

- Credit score Combine: Having a balanced mixture of secured and unsecured loans positively impacts your CIBIL rating. Nonetheless, having a better proportion of unsecured loans like bank cards and private loans might show to be unfavourable and reveals you as a dangerous borrower

- Period of Credit score Historical past: The length of your credit score historical past additionally impacts your credit score rating. You probably have used bank cards/loans for a protracted time frame and made well timed funds on it, it's going to favourably impression your credit score rating.

- Variety of Laborious Inquiries: Each time you apply for brand new credit score, the possible lender makes an inquiry in your CIBIL report. Such inquiries by lenders and monetary establishments are often called onerous inquiries and too many onerous inquiries might negatively have an effect on your credit score rating because it reveals you to be credit score hungry.

- Credit score Utilization Ratio: It's the quantity of credit score that you just use divided by the entire credit score accessible to you. A excessive credit score utilization ratio signifies the next dependency on credit score and a probably excessive reimbursement burden which negatively impacts your credit score rating.

Understanding the CIBIL Rating & CIBIL Report

CIBIL Rating is a Three digit rating, ranging between 300 and 900 which is calculated utilizing the credit score historical past discovered within the CIBIL report. It displays an individual’s credit score behaviour-his credit score reimbursement historical past, frequency of making use of for loans, bank cards, and many others. A rating nearer to 900 is taken into account to be extra appropriate for availing new credit score as in comparison with a rating nearer to 300.

CIBIL Report is a monetary doc which reveals a person’s credit score behaviour/credit score historical past with respect to all types of credit score and lending establishments. This report contains 5 key sections - CIBIL rating, private data, contact data, credit score account data and enquiry data. Your CIBIL report doesn't take into accounts some key monetary knowledge reminiscent of your financial institution steadiness, annual wage, financial savings, investments, utility payments paid or due, and many others.

How CIBIL Rating impacts your Mortgage Eligibility?

CIBIL rating is among the first issues that lenders have a look at when evaluating your mortgage software. As soon as a mortgage software is submitted to the lender, the lender checks the CIBIL rating and report of the applicant. It really works as a form of first impression for the lender. In case the CIBIL rating is low, the lender would possibly reject the appliance with out contemplating it additional. If the CIBIL rating is excessive, the lender would possibly look into different particulars to find out if the applicant is credit score worthy. Thus, a very good credit score rating will increase the probabilities of your mortgage software being accepted.

The upper your CIBIL rating higher are you probabilities of being accepted for a brand new mortgage or bank card. Nonetheless, CIBIL rating just isn't the one determinant of an individual’s capacity to safe new credit score. Lenders additionally take into accounts your debt to earnings ratio, your employment historical past, applicant’s occupation, and many others. earlier than approving/rejecting a mortgage software.

How CIBIL rating impacts your Credit score Card Eligibility?

CIBIL rating is among the first issues that banks search for whereas providing a brand new bank card to an individual. Usually a rating nearer to 900 is taken into account to be a very good rating. It signifies you could handle your credit score effectively and have a very good credit score historical past. Whereas folks with decrease CIBIL scores will also be eligible for a bank card they are usually perceived as increased danger debtors and subsequently could also be charged the next rate of interest and provided decrease credit score restrict. That stated, CIBIL rating just isn't the one determinant of an individual’s capacity to get accepted for a brand new bank card.

Simple Methods to Enhance your CIBIL Rating

Some methods to enhance your CIBIL rating are given beneath:

- Make well-timed fee of your bank card and mortgage dues. It reveals accountable credit score behavior and reimbursement capacity.

- Keep a very good credit score mixture of secured and unsecured credit score. Having an excessive amount of unsecured credit score like private loans and bank cards makes lenders take into account you as a dangerous borrower and will lower your credit score rating.

- Test your credit score report for administrative errors and fraudulent utilization of knowledge/data. These have to be reported and rectified in a well timed method. This may increasingly assist to spice up your credit score rating.

- Cut back your credit score utilization. Try to restrict your credit score utilization to a most of 30% of your accessible credit score restrict. Spending greater than 30% of the accessible credit score reveals extreme reliance on credit score and reduces your credit score rating.

- Try to get banks to extend the credit score restrict in your card. This doesn't imply that you just begin spending extra or improve your bills. However, quite it helps to lower the credit score utilization ratio because the accessible credit score restricts will increase however the utilization stays the identical. This has a optimistic impression in your credit score rating.

- Keep away from making too many new bank card/mortgage purposes and inquiries inside a brief time frame (or making inquiries with a number of lenders on the identical time). It could improve the variety of onerous inquiries in your credit score report and adversely have an effect on your credit score rating.

- Make sure you repay your money owed as an alternative of settling them. Although settling might scale back the debt burden, it reveals an lack of ability to repay your money owed and will thereby adversely have an effect on your credit score rating.

Parts of CIBIL Report

A CIBIL report or a Credit score Data Report (CIR) incorporates an individual’s credit score fee historical past throughout numerous varieties of loans and credit score establishments over a time frame. It's used to derive the CIBIL rating. The important thing elements of CIBIL report are given beneath:

- CIBIL Rating: The CIBIL report displays an individual’s credit score behaviour (credit score historical past) which is used to calculate the CIBIL rating. The CIBIL rating ranges between 300-900. A rating nearer to 900 is taken into account to be a very good rating.

- Private Data: The CIBIL report additionally incorporates private data reminiscent of your title, gender, date of beginning and identification numbers like passport quantity, PAN and voter’s quantity.

- Contact Data: This part incorporates your phone numbers and addresses. Most Four addresses may be talked about.

- Account Data: The small print of your credit score amenities like title of lenders, form of credit score amenities (overdraft, private, dwelling, and many others.), account numbers, mortgage quantity, month on month report of your funds, and many others. are there on this part.

- Enquiry Data: Every time you apply for a mortgage or bank card, the respective monetary establishment or financial institution accesses your CIBIL report. These inquiries are listed within the report and comprise the seller’s title, quantity of credit score utilized, date of software of credit score and credit score sort.

The best way to Obtain CIBIL Report?

You may obtain your CIBIL report by following the steps given beneath:

- Go to https://www.CIBIL.com/freeCIBILscore.

- Click on on ‘Get Yours Now’.

- Enter private data like your title, date of beginning, contact quantity, choose the ID sort and ID quantity, and many others. and create your individual username and password.

- An OTP is distributed to you to confirm your identification or further particulars could also be requested to substantiate your identification.

- As soon as your identification is verified, you'll be able to test your CIBIL rating and obtain the CIBIL report.

Advantages of sustaining a very good CIBIL rating

Although CIBIL rating just isn't the one factor that lenders have a look at when contemplating a mortgage or bank card software, it's arguably one of the necessary ones. Some benefits of sustaining a very good CIBIL rating might embrace:

- Better probabilities of mortgage purposes being accepted, as a excessive credit score rating signifies increased credit score worthiness and decrease danger for the lender

- You usually tend to obtain decrease rate of interest loans

- Loans and bank cards are accepted shortly and simply

- Entry to pre-approved loans

- Capacity to avail increased bank card restrict

- Low cost on processing charges and different fees

Client CIBIL Bureau vs Industrial CIBIL Bureau

Client CIBIL bureau maintains credit score data of people whereas business CIBIL bureau maintains credit score data of firms. The previous offers the credit score reimbursement historical past of people throughout a number of mortgage varieties and lenders, whereas the latter conveys the credit score worthiness of firms. The patron bureau gives CIBIL credit score studies for people whereas the business bureau gives CIBIL rank to companies.

Distinction between CIBIL Report and CIBIL Rank

![]()

Cellular Apps to Test Your CIBIL Rating

Lots of the official companions of TransUnion CIBIL present people the choice to test their CIBIL report and rating by way of cellular apps. You should utilize the Paisabazaar mobile app to test your CIBIL rating and obtain your CIBIL report totally free with month-to-month updates.

CIBIL Buyer Care

You may contact TransUnion CIBIL’s buyer care executives via the next means:

- By Telephone: You may name at +91-22-6140-4300 (Mon-Fri between 10:00 AM to 06:00 PM)

- Fax: You may contact the corporate’s buyer care via fax at +91 - 22 - 6638 4666

- Go to the Company Workplace/Write to the Firm: You too can go to the company workplace or write to the corporate to get your queries answered/grievances redressed. The registered deal with is:

TransUnion CIBIL Restricted

One World Middle, 19th Flooring, Tower 2A and 2B,

841, Jupiter Textile Mill Compound, Senapati Bapat Marg,

Decrease Parel, Mumbai – 400 013

Contact On-line: You too can contact the corporate’s buyer care executives on-line. For this merely go to https://www.CIBIL.com and click on on ‘Contact Us’. Underneath ‘To Contact Us On-line’ part choose ‘Click on right here’. Enter the required particulars and your question and click on on ‘Submit’.

FAQs

Q1. How is my CIBIL Rating calculated?

Your CIBIL rating is calculated utilizing a posh statistical mannequin, which is a proprietary enterprise secret of TransUnion and CIBIL and therefore, not accessible to most people. The statistical mannequin identifies a number of variables in your credit score report in an effort to calculate credit score rating.

Q2. Will my CIBIL rating ever change?

Sure. Your CIBIL rating relies on a number of elements, reminiscent of all present and former loans/bank cards, fee historical past of credit score devices, variety of excellent loans/bank cards and card utilization ratio. A change in any of those elements can deliver a couple of change in your CIBIL rating. Thus, little observed elements, reminiscent of late funds and maxing out your bank cards, in addition to extra noticeable elements that embrace a brand new dwelling mortgage or automobile mortgage can even change your credit score rating.

Q3. Is CIBIL the one one who gives a CIBIL Rating?

Sure. CIBIL Rating is supplied solely by TransUnion CIBIL (Credit score Data Bureau (India) Restricted) and it's one among Four bureaus that present credit score scores and credit score data studies to people all through India. Aside from CIBIL, numerous different credit score reporting companies which are at the moment licensed to function in India are Experian, Equifax and CRIF Excessive Mark. Every bureau gives its self-generated credit score studies and scores respectively to its shoppers and members worldwide.

This fall. Is the Credit score Data Report as identical because the CIBIL Rating?

No. Your rating is just part of your credit score report, which is also called the CIR (Credit score Data Report). Aside out of your credit score rating, your CIBIL report additionally contains the main points of assorted loans and bank cards that you've had over the previous 5 to 7 years. The small print associated to your bank card/mortgage embrace credit score limits, credit score reimbursement observe report, variety of credit score checks carried out by potential lenders up to now, and many others. Similar to a medical report gives particulars concerning your bodily well being, equally, a credit score report gives the main points about your monetary well being.

Q5. Can everybody entry my CIBIL Rating?

No. Your CIBIL rating is confidential private data that solely you or a couple of licensed entities (in your consent) are allowed to entry. These licensed entities can entry your credit score report solely below particular circumstances, as an illustration if you apply for a brand new mortgage or bank card and are legally not allowed to share any data with any unauthorized third occasion. Some licensed entities that may entry your CIBIL rating/report embrace monetary establishments and banks, who're trusted CIBIL members.

Q6. The best way to test CIBIL Rating totally free?

As per the RBI’s directives, the credit score bureaus shall give entry to FFCR (Full Free Credit score Report) as soon as in a yr to everybody whose credit score data they maintain. You may request to your free credit score report anytime as soon as in a yr from CIBIL’s official web site.

Q7. How did CIBIL find out about my loans and bank cards?

CIBIL works on a reciprocity precept i.e. CIBIL members can entry the information of CIBIL provided that the members (Banks and NBFCs) present TransUnion CIBIL with the information of their debtors. On this method, all of your mortgage and bank card data will get reported to CIBIL by your current lenders and these kind the idea of your report and rating. The identical logic holds true for credit score scores ready by Experian, Equifax and CRIF Excessive Mark.

Q8. Would checking my CIBIL Rating result in its lower?

No. In case you test your credit score report or CIBIL rating, it's thought-about to be a “delicate inquiry” and one of these test doesn't have an effect on your CIBIL rating in any means. This holds true even if you happen to’re checking different credit score bureau’s credit score rating or report. Nonetheless, the “onerous inquiries” made by banks and monetary establishments in your credit score report and rating might adversely have an effect on the credit score rating.

Q9. Does CIBIL Rating have an effect on my probabilities of getting a brand new mortgage or bank card?

At current, your credit score rating whether or not reported by CIBIL, Experian, Equifax or CRIF Excessive Mark, is among the key elements that decide your eligibility to get a brand new credit score product. Totally different banks and NBFCs have totally different cut-off standards in offering new credit score merchandise. Sustaining a excessive credit score rating (nearer to 900) positively improves your probabilities of getting approvals on further credit score merchandise. Nonetheless, CIBIL rating (or credit score rating) just isn't the one standards that determines an individual’s eligibility to safe new credit score. Lenders additionally have in mind different elements like your debt to earnings ratio, credit score and employment historical past, their very own inside standards, and many others. earlier than making lending selections.

Q10. What's the minimal CIBIL rating required for any sort of mortgage?

There is no such thing as a evident knowledge accessible at current concerning what's the minimal, good or excessive CIBIL rating for getting loans or bank cards. As talked about earlier, the CIBIL rating vary is from 300 to 900, subsequently the nearer you're to 900, the higher your probabilities of approval. In any case, the discretion of offering approvals on loans or bank cards solely relies on banks, NBFCs and monetary establishments.

Q11. How do I improve/enhance my CIBIL Rating?

CIBIL rating relies in your credit score historical past and it can't be elevated in a single day, it doesn't matter what a self-styled CIBIL rating enchancment company would possibly let you know. It begins with paying your bank card dues and EMIs on time, whereas additionally requiring you to attenuate your excellent debt.

Q12. Why is a bank card account that I already paid off and closed nonetheless on my report?

Your present lenders report your mortgage/bank card standing to CIBIL periodically and these particulars get mirrored in your report over time. Subsequently, if you happen to shut out a mortgage or bank card account this month, it may be a few months earlier than the data will get mirrored in your credit score report. Different causes of such discrepancy could also be a reporting error as a result of financial institution or NBFC that you just took the mortgage or bank card from or you might be a sufferer of identification theft.

Q13. What occurs if my CIBIL Report has errors?

In case you discover errors in your CIBIL report, you'll be able to request CIBIL to right it via their Dispute Decision process. As a part of this course of, you'll be required to submit supporting paperwork, reminiscent of financial institution NOC, mortgage settlement letter and in addition nominal price to get your information up to date.

Q14. Can CIBIL delete or change my credit score data by itself?

No. CIBIL doesn't have the authority to delete or make adjustments in your credit score report by itself. They're solely concerned with collating the info as supplied by the member banks and NBFCs. Nonetheless, in instances of credit score report disputes, CIBIL will make adjustments to your credit score report supplied there's enough documentary proof to indicate that an error has truly occurred. Nonetheless, the involved banks or NBFCs must present the mandatory clearance earlier than CIBIL make such adjustments.

Q15. What's CIBIL 2.0?

Over the previous few months, TransUnion CIBIL has been shifting to a brand new scoring mannequin in an effort to be extra related with altering buyer credit score knowledge and profiles, in addition to present financial developments. This new scoring mannequin has been termed as CIBIL 2.0. The principle change is an task of danger index from 1 to five to people with comparatively new credit score historical past, i.e. lower than 6 months. The upper the numeric worth of the danger index, the decrease is the perceived danger of default.

At the point when we converse with customers of new or set up organizations it appears they are quite often discussing deals, so the capacity to comprehend and zero in on the distinctions in their benefits and money changes is vital. Financial coach near me

ReplyDeleteI'm glad to see the great detail here!. 신용카드 현금화

ReplyDeleteIn case you are contemplating recruiting a credit fix administration to tidy up your awful credit report, you better take notes on the accompanying unique report:need credit

ReplyDeletesolve credit

I just found this blog and have high hopes for it to continue. Keep up the great work, its hard to find good ones. I have added to my favorites. Thank You. 신용카드 결제 현금화

ReplyDeleteI’ve been searching for some decent stuff on the subject and haven't had any luck up until this point, You just got a new biggest fan!.. 콘텐츠 이용료 현금화

ReplyDeleteI appreciate everything you have added to my knowledge base.Admiring the time and effort you put into your blog and detailed information you offer.Thanks. 정보이용료 현금화

ReplyDelete